Summer Heatmap Gets Redder

Summer Heatmap Gets Redder

Final Month of Q2 2019 Left To Go, Cash Looks Cool

This market seems ripe for a bounce given the recent declines of May 2019. (No, no, we will refrain from that “Sell in May” phrase. No need for that.)

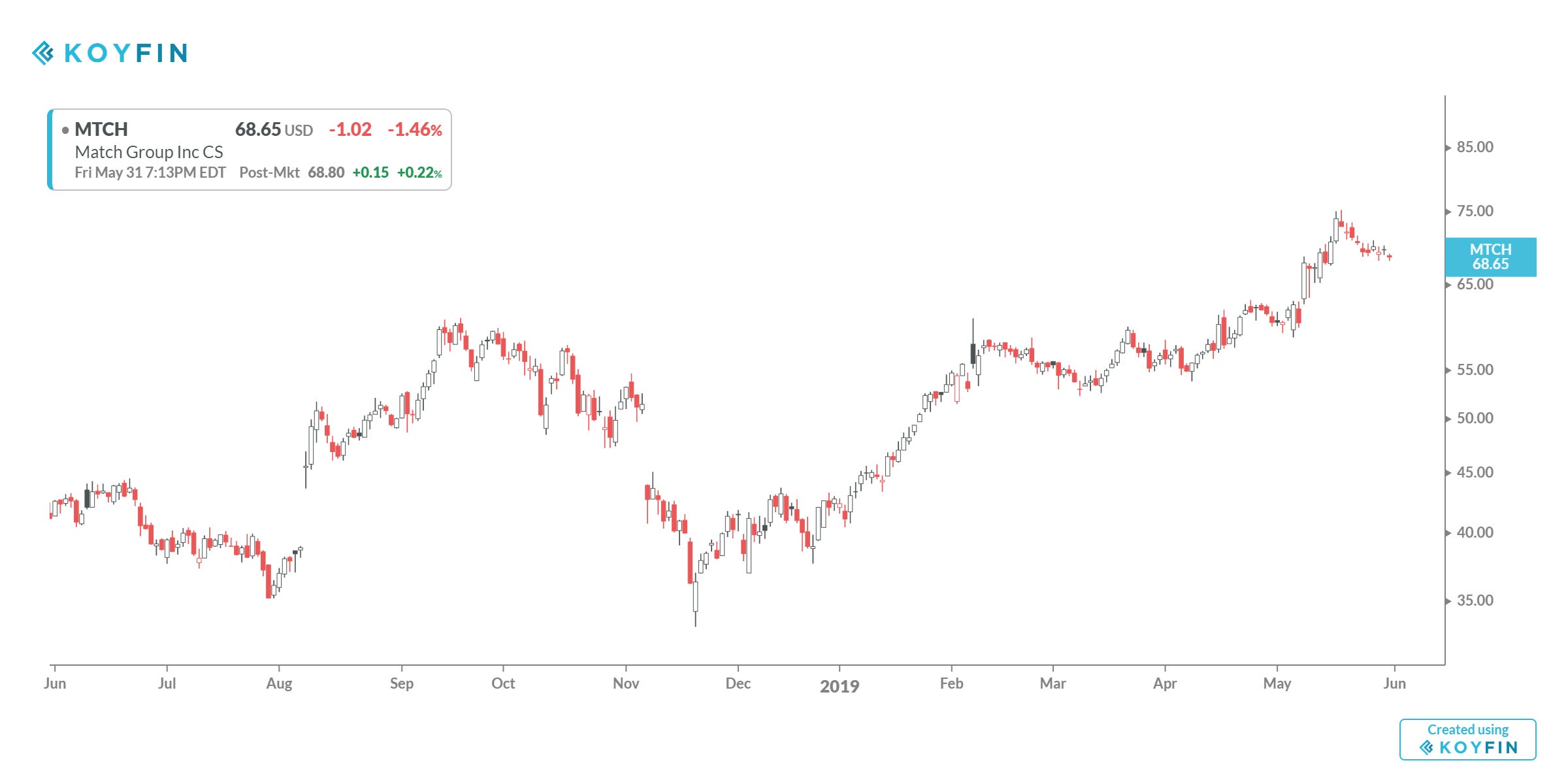

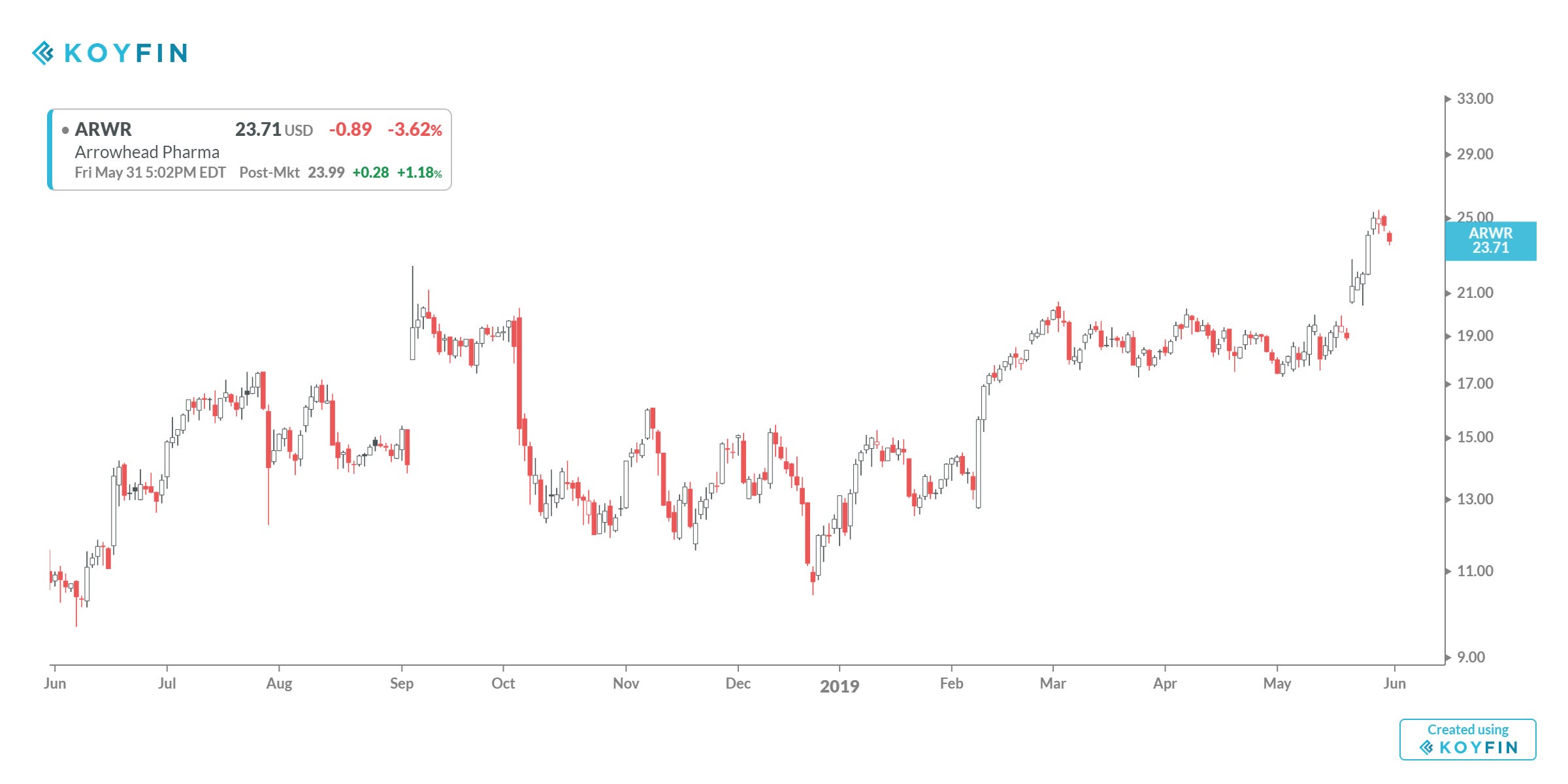

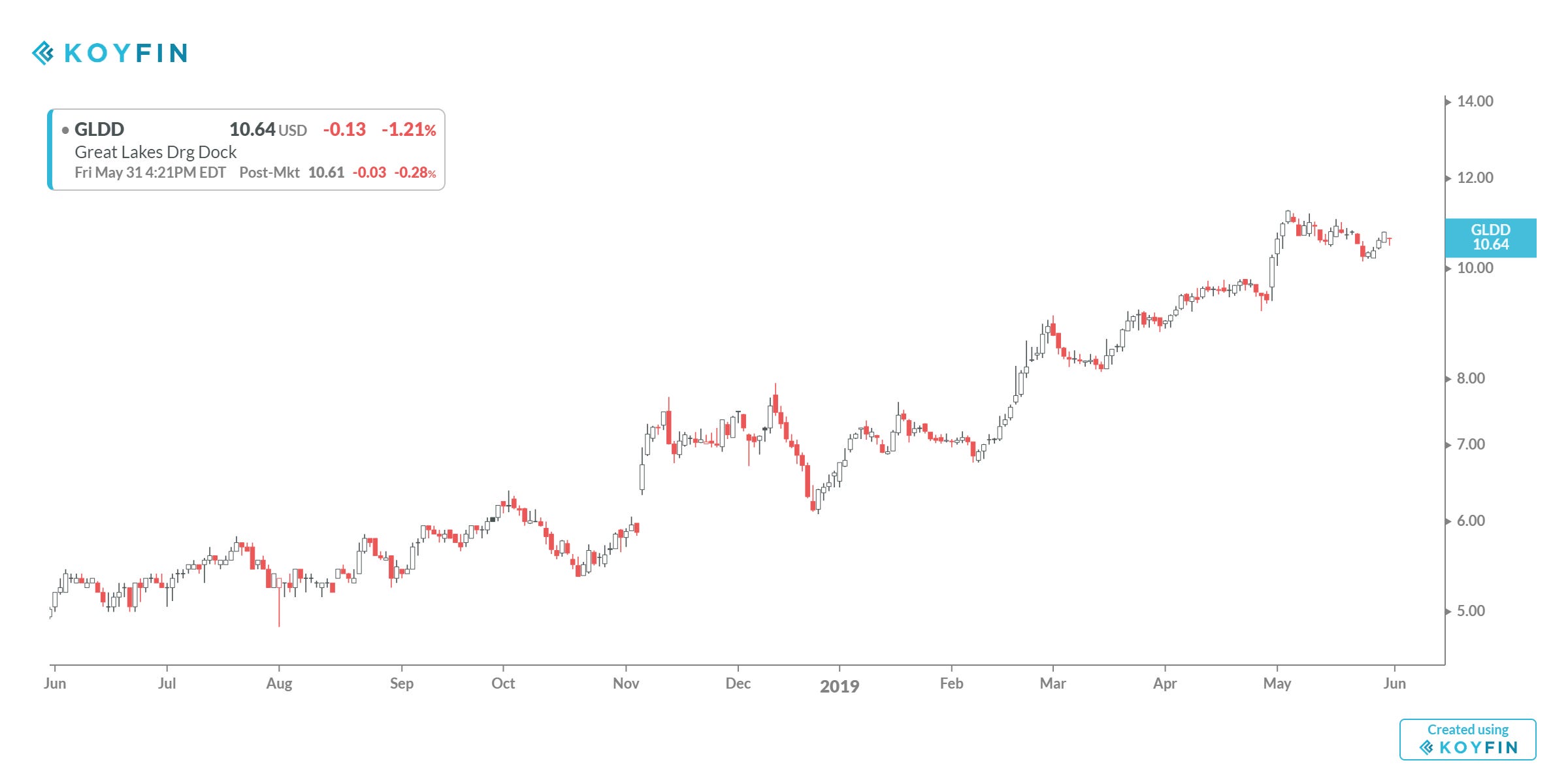

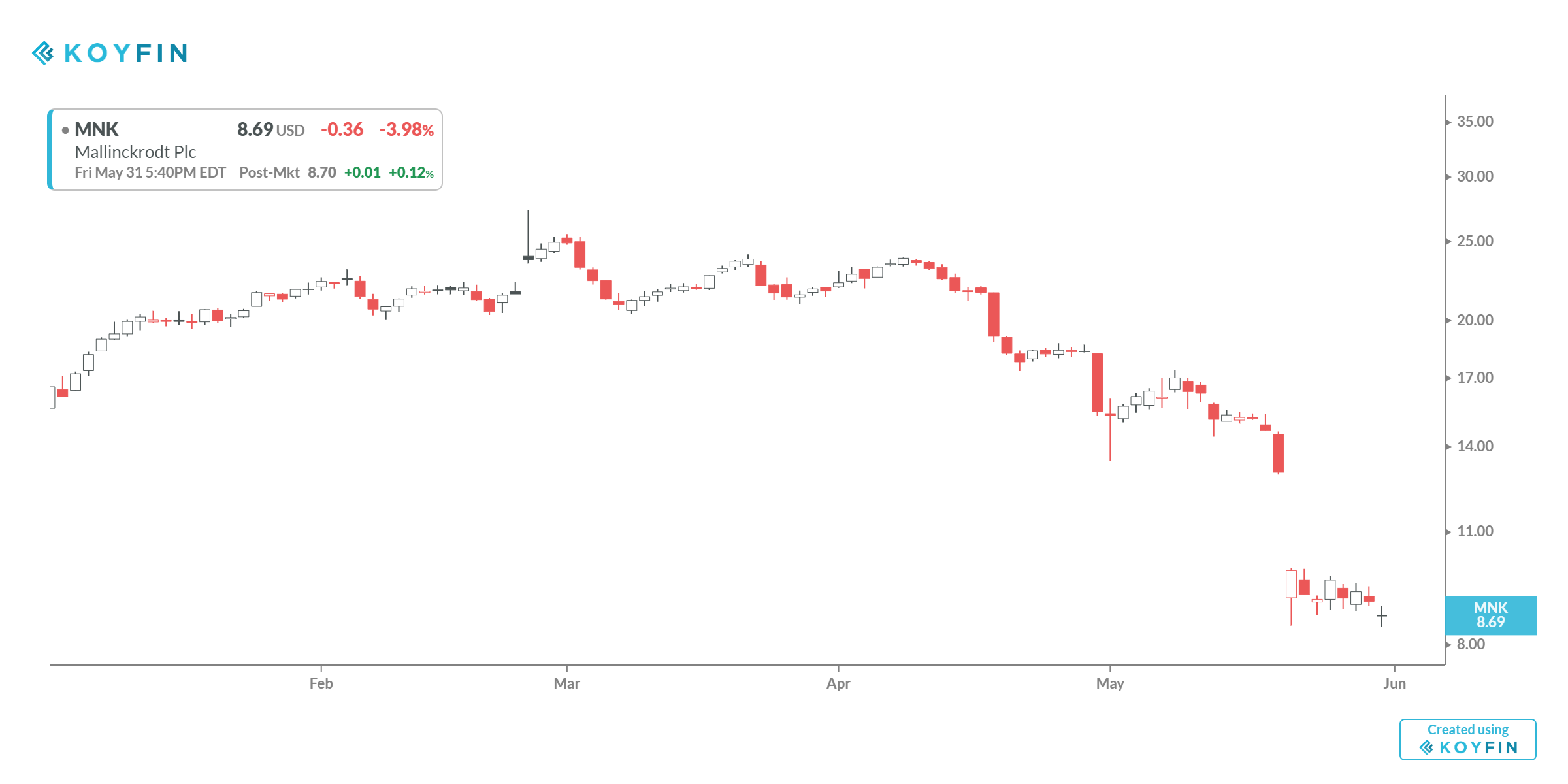

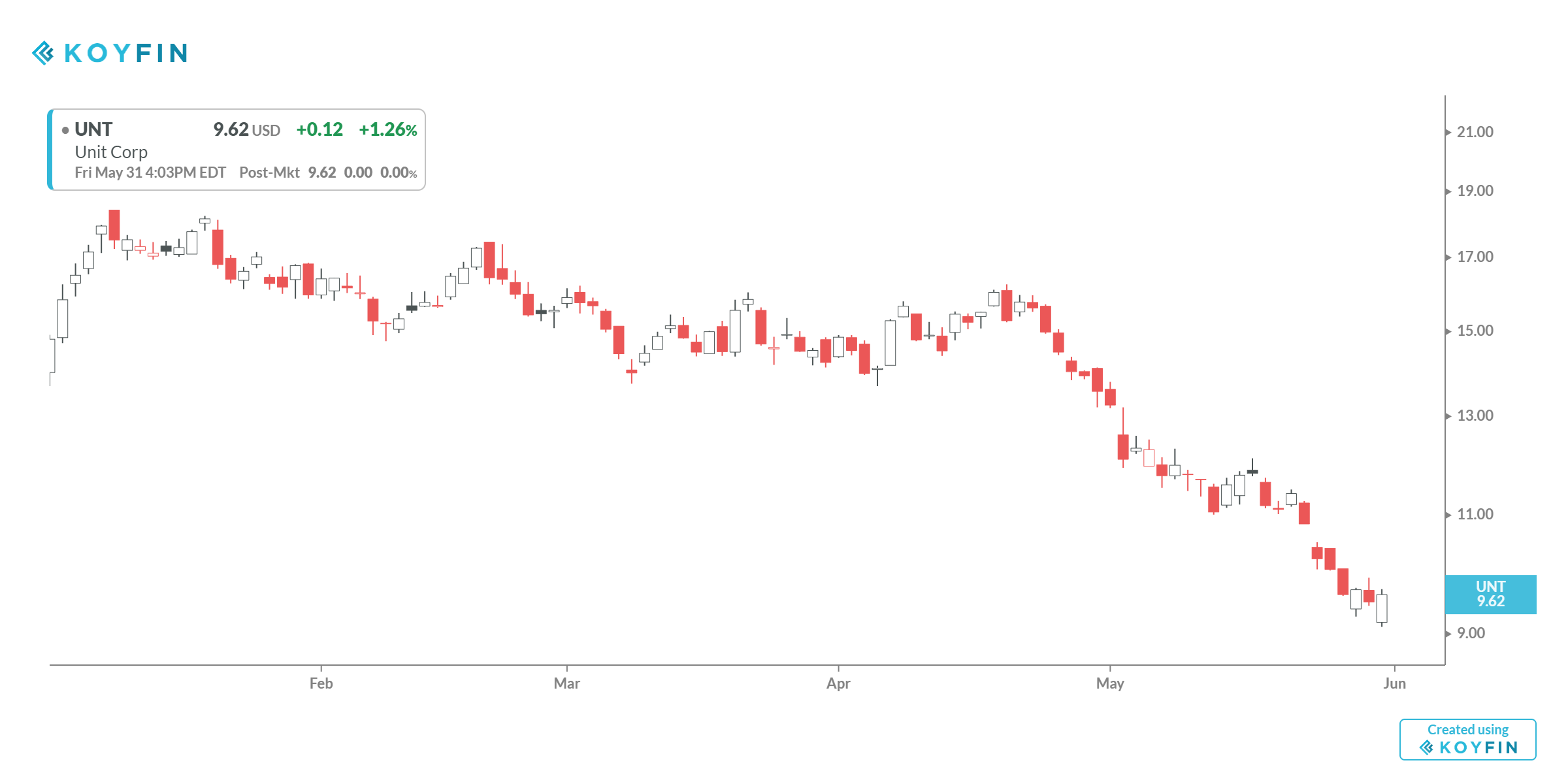

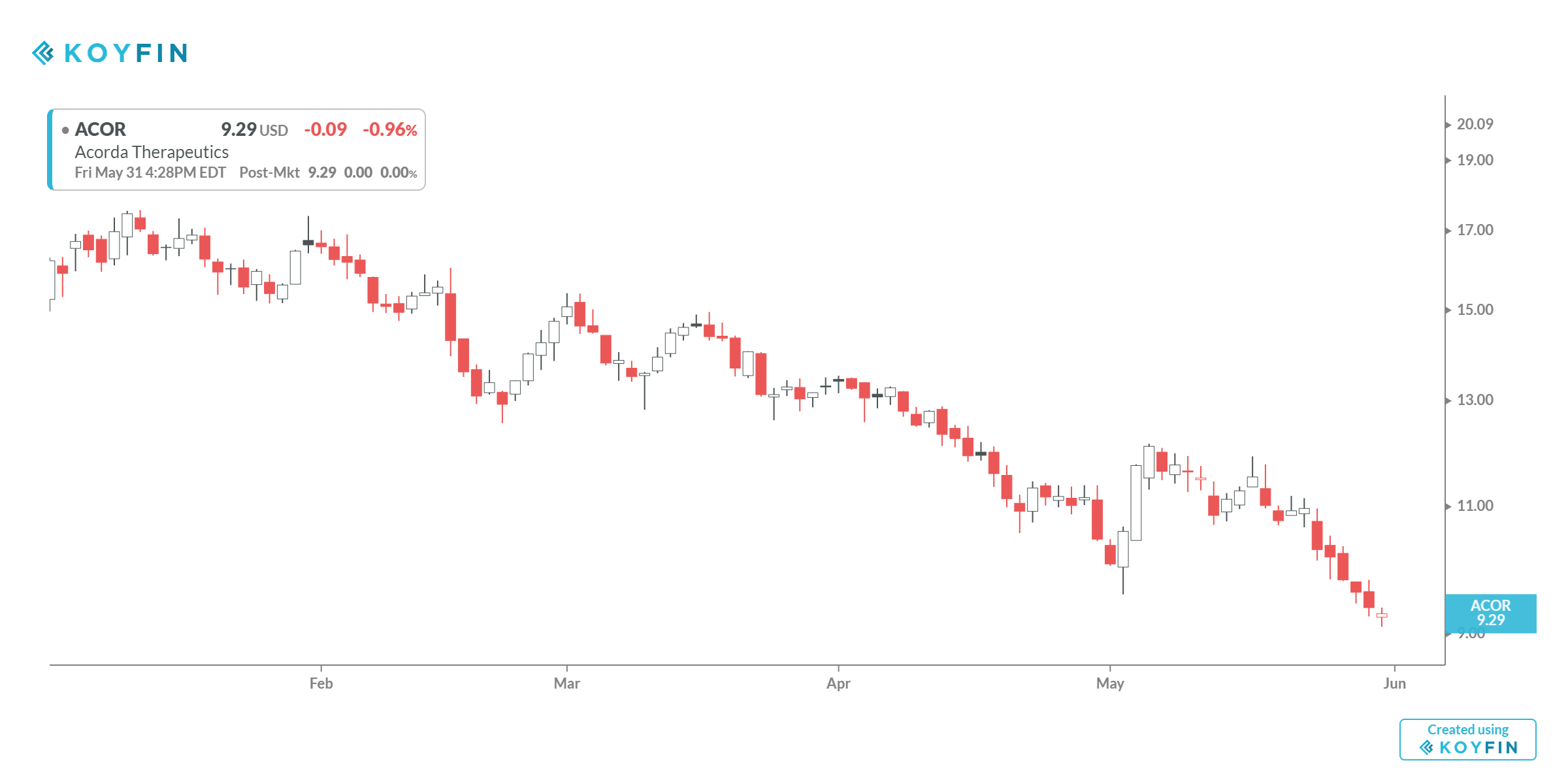

Let’s note that the profits this week from the SELL side continue to get stronger, it’s a bit much a bit too quickly - no telling how much more to come. Share below is this week’s latest “top down summary”. Its still about 500+ ideas, with most of the notional gains coming from the SELL ideas side. This was telegraphed in the last couple of weeks of “top down” summaries.

Here is the prior week’s Top Down summaries update for context on trend.

These “top down summaries” are not elegant but they tell the story in workman-like fashion that the broader market, as viewed through trend trading’s price following prism, of a market under pressure. Let us look at the Top 20 LONGS, charts & summary, first and then move on to the Top 20 SELLS.

Warning: “chart crimes” here - it’s all simple charts, not proper log charts, to hint just for direction.

The below Top 20 LONGS has the entry price and week, the most recent weekly close, and the simple return and a “risk / share” figure (how much you can risk losing per idea per share as well an estimated stop loss exit price to cut and run.

This list will be updated on a regular basis as a Koyfin dashboard

https://www.koyfin.com/myd/5c8de099e264be29ac997f1d

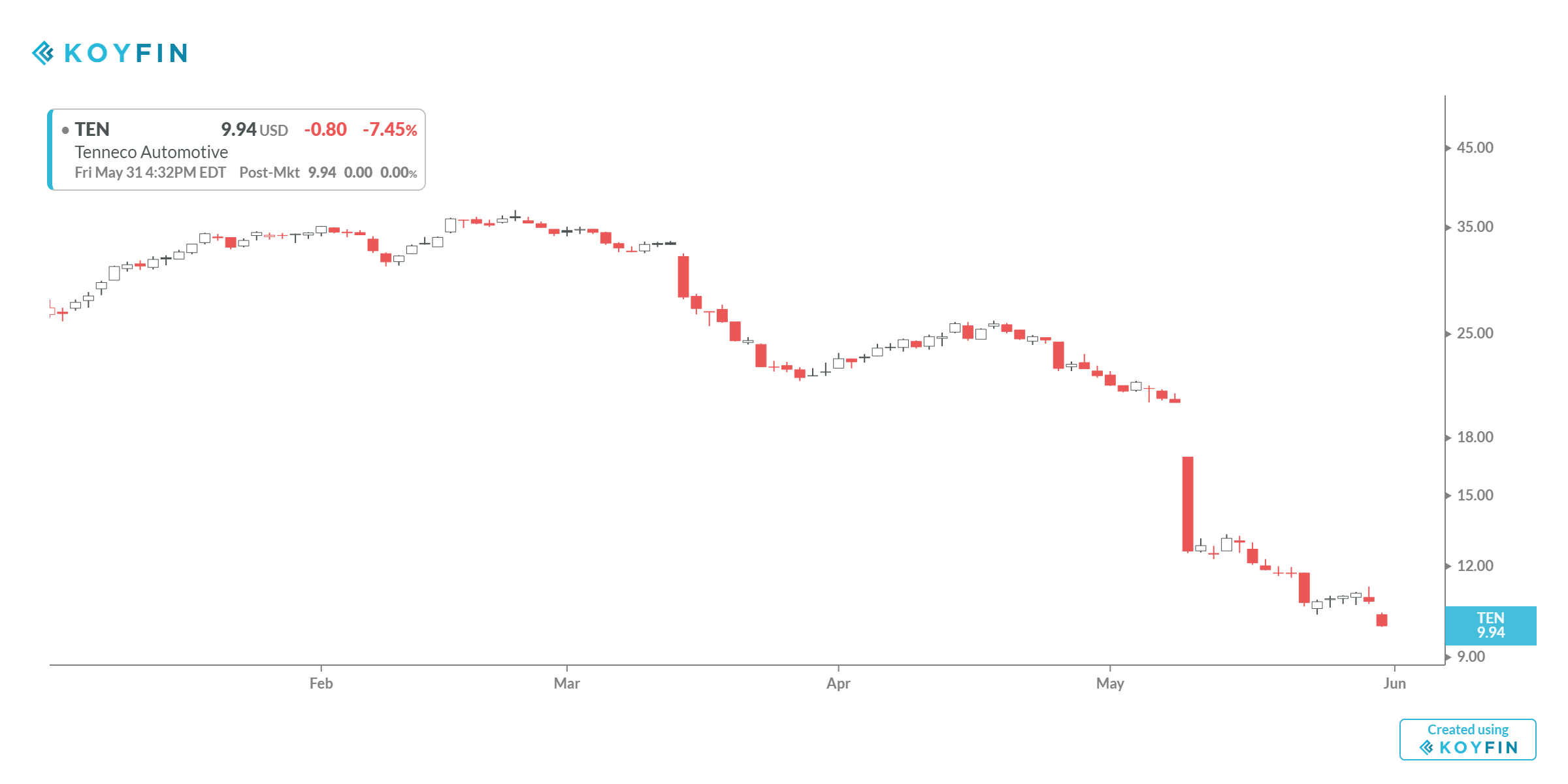

And now for the Top 20 SHORT/SELL charts and top down summary chart.

It’s not pretty but it’s useful to be alert as to which groups are in decline or under pressure. Here is the Koyfin Top 20 Sell list which will also be updated regularly.

https://www.koyfin.com/myd/5c8de2b7e264be4536997f61

It’s pretty brutal action over the past month and we must be mindful of our risks.

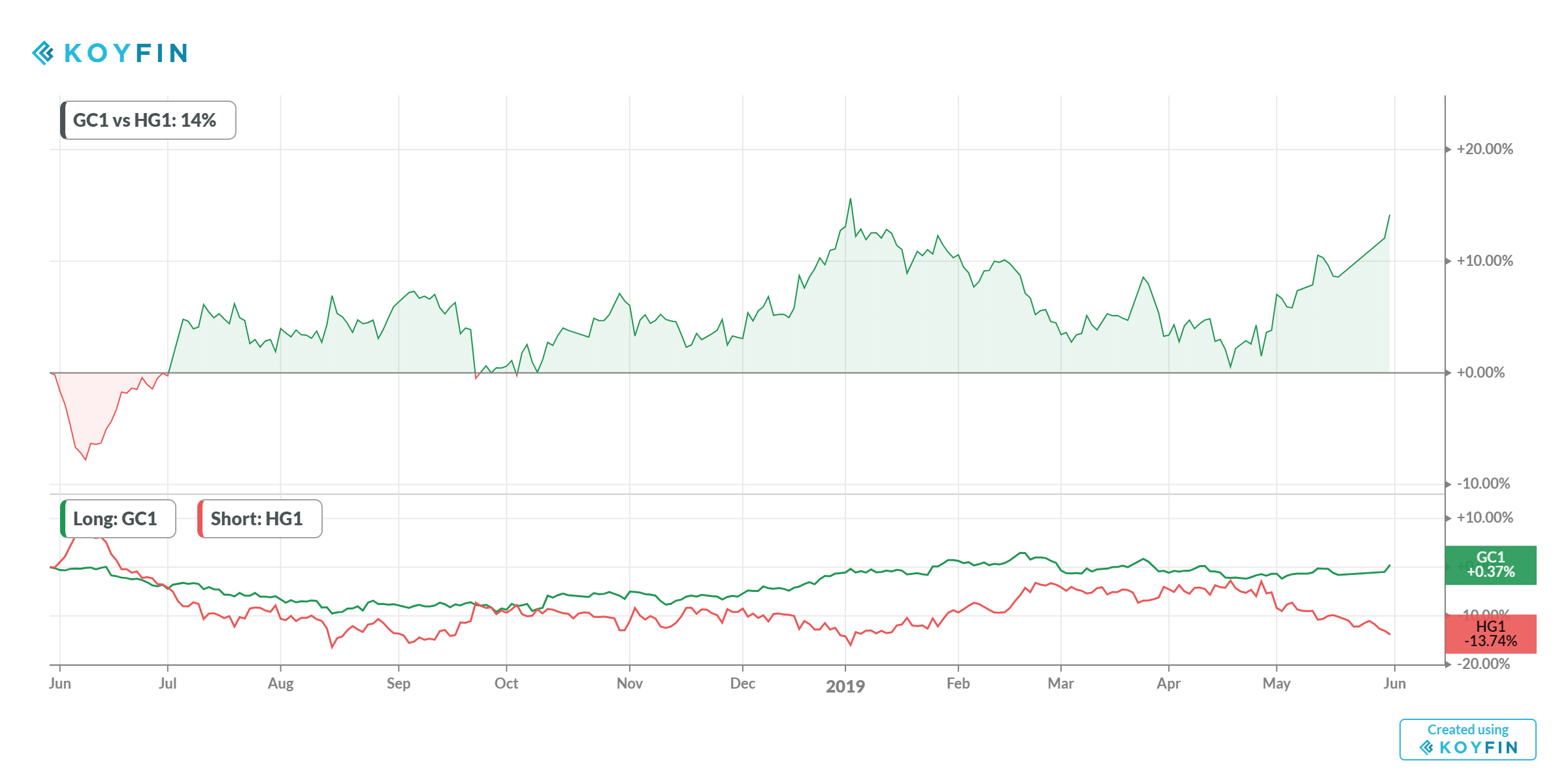

Let’s use Koyfin for a few more top down views.

Gold vs. Copper - a primitive metal traders’ POV on trends - NOT good.

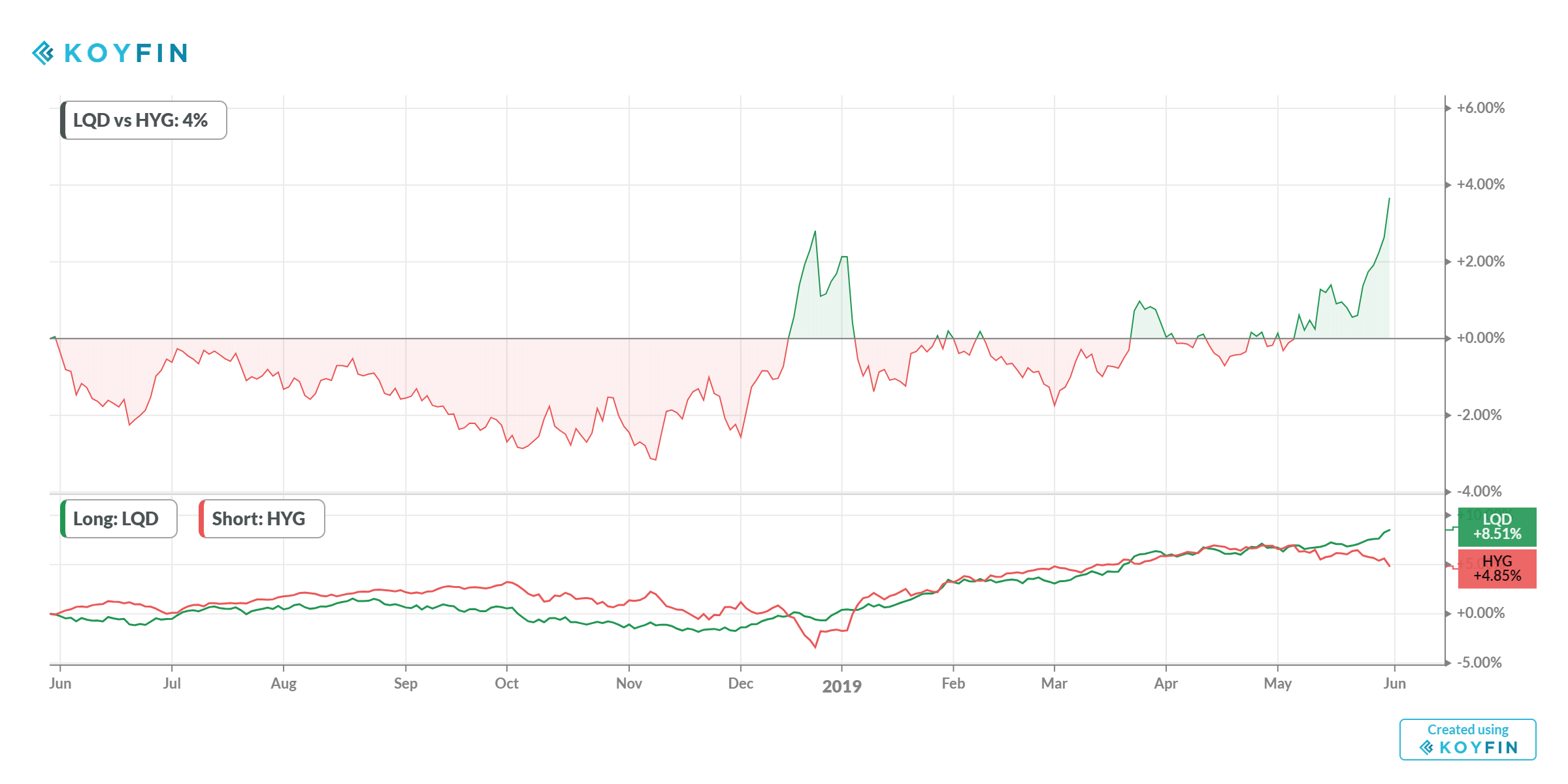

LQD vs. HYG or Liquid Investment Grade vs. High Yield - Not Nice.

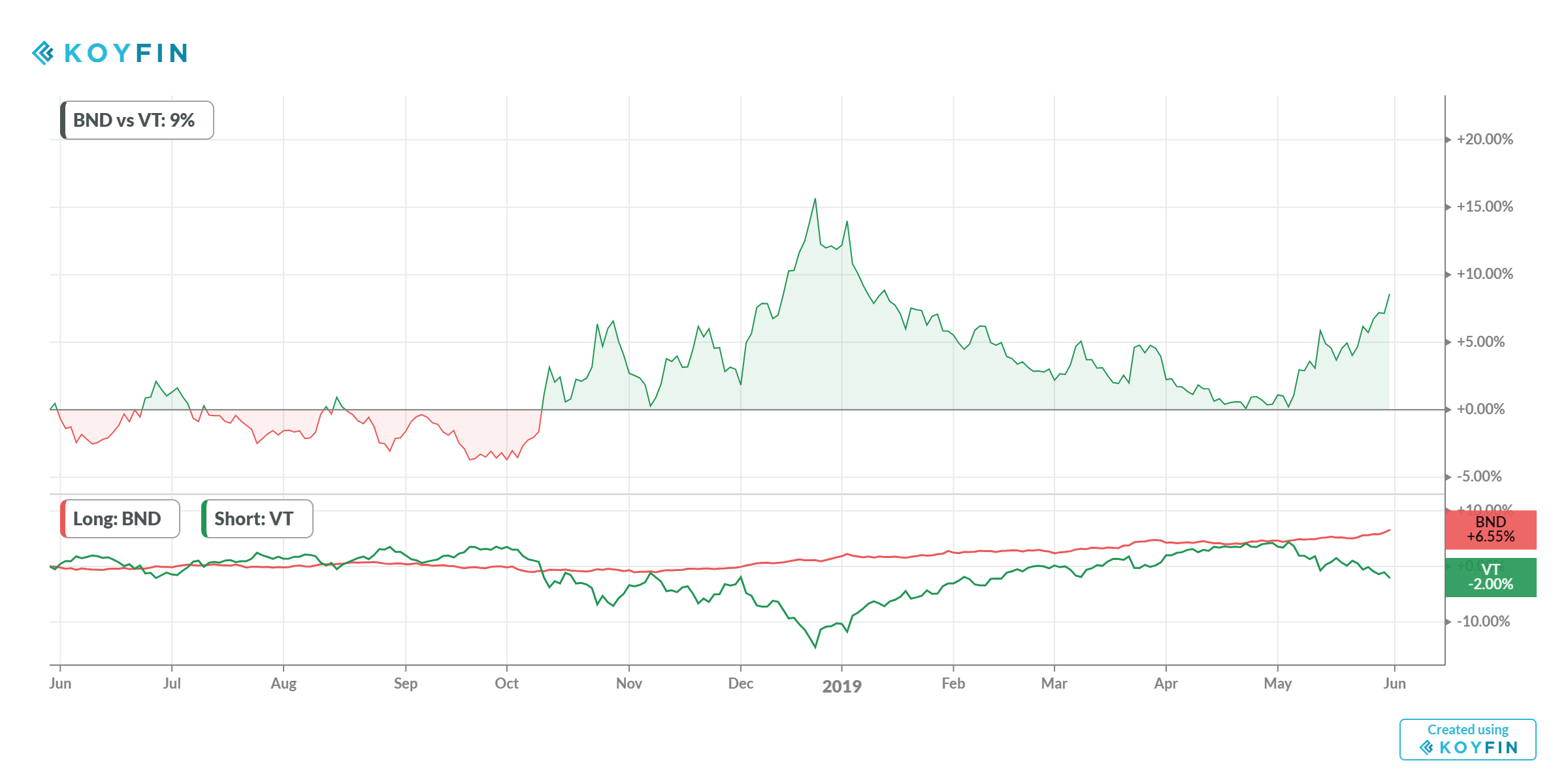

VT vs. BND = Total BOND vs. Total Equity proxies - NOT pleasant

And now for some more conventional trend charts

We’re back to not pretty like Q4 2018 to put it bluntly. Let’s hope that changes.