Huawei Supply Chain Train Derailed

Notes on an evolving large tense situation

Huawei Technologies Co. Ltd., pronounced “Wah Way”, is the world’s largest telecom network equipment maker and second largest mobile maker with 170,000+ employees.

Huawei bills itself as an employee owned private company but is financially tied at the hip with the Chinese government. It’s now at the center of escalating tensions prompted by a series of tariffs imposed by the Trump administration on Chinese goods since last year as part of a promise to lower the U.S.-China trade deficit.

In 2018, the U.S. exported 120B USD in goods to China and China exported 540B USD in goods to U.S. - this meant a U.S. “trade deficit” of negative 420B USD because the U.S. sold less than it bought from China.

Some charts from the Financial Times, to help us visualize the scale of the U.S. trade deficit.

As one of the world’s largest telecom equipment makers with ties to the Chinese government, Huawei would naturally be caught up in a drive to lower the trade deficit but it also has issues of its own which made it a target.

The Trump administration is not only intent on lowering the trade deficit, it’s also focused on allegations of tech intellectual property theft by China and U.S. tech companies being compelled to share their “IP” as part of closing deals in China.

A fascinating podcast from Vice.com highlighted a reporter’s surreal visit to learn more about Huawei in the midst of a “digital cold war” which has been marked with incidents including:

- The Dec.1, 2018 arrest in Canada of Huawei’s CFO Meng Wanzhou (also the daughter of Huawei’s founder), as part of an indictment of Huawei for selling U.S. technology to Iran.

- an indictment for a theft of robot arm mobile phone testing tech from T-Mobile

This digital cold war’s escalation as reported by the Economist:

“ON MAY 20TH … some of the world’s most prominent technology companies—Google, Intel and Qualcomm—had stopped selling software, hardware and licences for intellectual property to Huawei, a Chinese manufacturer of phones and networking gear.”

“This followed an announcement by the American government on May 15th that it was banning the export of American technology to Huawei unless companies got a special licence from the Department of Commerce.”

Many U.S. companies that were suppliers to Huawei are now caught in the middle of this situation. And there is a reason to suspect that they may stay that way for a while.

There are reports that Huawei made preparations for this “war” and amassed enough inventory to carry it through for several months. It also has an Achilles Heel however since it has no immediate solution for the loss of licenses for both Google’s Android OS. and ARM Holdings’ Semiconductor IP which underlie a large part of Huawei’s hardware. U.S. suppliers will suffer as well too since future sales to Huawei have been pulled into the present due to these advanced orders. Even if the U.S. ban on Huawei was lifted, sales for many suppliers have already been booked.

The real worry for investors is what happens to U.S. suppliers’ earnings over the next couple of years even if a negotiated settlement is made with Huawei.

The U.S. bull market has also been a bull market in tech companies and many of them are suppliers to Huawei.

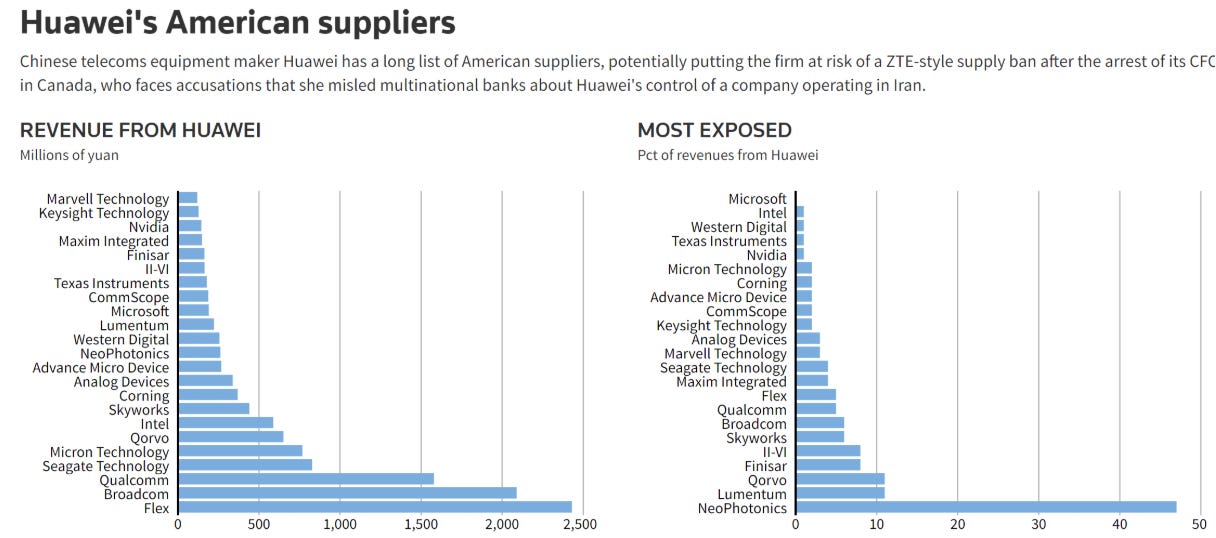

Consider the tech companies whose revenue includes business from Huawei:

Flex, Broadcom, Qualcomm, Seagate Tech, Micron Tech, Qorvo, Intel, Skyworks, Corning, Analog Devices, AMD, NeoPhotonics, Western Digital, Lumentum, Microsoft, CommScope, Texas Instruments, II-VI, Finisar, Maxim Integrated, Nvidia, Keysight Tech., Marvell Tech.

U.S. investors may not have asked for these headaches but as tech company investors have now been pulled into it.

Look at some of the relevant stock charts for directly impacted companies in this situation. Since we are focused on “trend trading”, it is clear the trend is lower.

Unless investors have a long time frame and/or are “averaging down” investment positions, they should be wary about raising their exposure to tech companies. They are trending lower for a variety of reasons which include an open-ended trade war and cloudy prospects over future revenues.

A footnote:

One apparent casualty includes the delisting of a Chinese semiconductor stock

$SMI “Semiconductor Manufacturing International Corporation ("SMIC";NYSE: SMI; SEHK: 981), one of the leading foundries in the world, is Mainland China's largest in scale, broadest in technology coverage, and most comprehensive in semiconductor manufacturing services.”